|

V-GRO is an outcome of our research to identify undervalued, yet strong performing companies in the Indian economy.

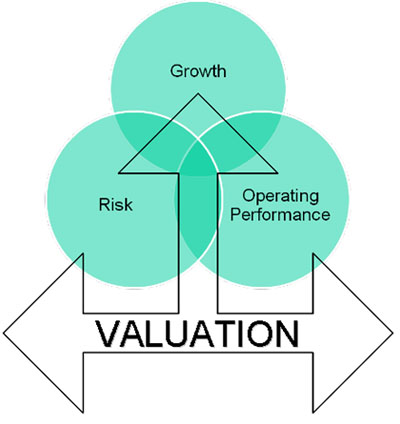

V-GRO assesses the Valuation of a company and puts it in perspective with the key drivers of value –the Growth, Risk (both financial and business risk) and the Operating performance of the company. It essentially balances out the valuation expectations and the fundamental performance of the company. When applied to a large sample size, it generates the ‘buy’, ‘hold’ and ‘sell’ sets of companies – essentially provides a credible ‘bird’s eye view’ based on fundamental drivers of value creation and complements the insights of even the most talented individual analysts.

V-GRO clearly is different from the bulk of Street research, which tends to be based on one, an analysis of accounting metrics that may not truly reflect the economics of the business and two, on crystal ball predictions for the company, industry sector, the domestic economy and the global macroeconomic parameters. V-GRO is based on hard facts and the microeconomic performance of a company and juxtaposes it on the broad canvas of the opportunity set – it provides a good screen to identify and conduct further qualitative assessment of identified opportunities. It considers objective parameters to assess and define ‘Valuation’, ‘Growth’, ‘Risk’ and ‘Operating performance’ of the company. The secret sauce is its ability to assess performance expectations based on economic profit (or EVA) embedded in the valuations; the actual performance relative to expectations enables identification of ‘winners’, ‘losers’ and the ‘also ran’. While, V-GRO can be applied to both listed and unlisted companies, it is especially powerful for majority of listed companies that are thinly covered and ‘undiscovered’.

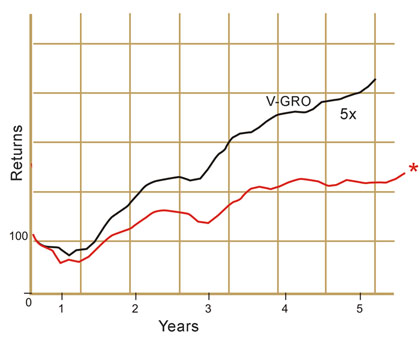

On an average the V-GRO portfolio (stress tested over a period of ten years) deliver about 4X to 5X returns in excess of the broad benchmark index over a period of about 5 to 6 years. The top deciles and quintiles deliver much higher returns.

The ‘V-GRO buys’ tend to outperform their fundamental performance expectations better than rest by about 5 to 1. In other words, there is a 5 times more chance of a ‘V-GRO buy’ company outperforming expectations than the rest of the companies.

Likewise, the ‘V-GRO sell’ companies tend to underperform by about 0.60X to 0.70X the broad benchmark and also underperform the expectations.

The ‘V-GRO buy’ companies typically have revenues in the range of INR 3 to 25 billion, market capitalization of about INR 2 to 15 billion, EBIDTA margins of about 7% to 15%, the capital turnover of about 1.5 to 3X, much in excess of broad industry and above they consistent outperformers on return on capital ‘expectations’

|